BayCoast Bank | Veteran Banking Team | Serving MA & RI

Buying a home is one of the biggest financial decisions you’ll make. For veterans and active-duty service members in Massachusetts and Rhode Island, there’s a question that comes up early in the process: should you use your VA loan benefit, or go with a conventional mortgage?

Both options have their place. But for most veterans who qualify, the VA home loan offers advantages that are genuinely hard to match — and many veterans either don’t realize what they’re entitled to, or assume the process is more complicated than it is.

Here’s a clear, honest comparison of VA loans vs conventional loans so you can go into the homebuying process knowing exactly what your options are.

What is a VA loan?

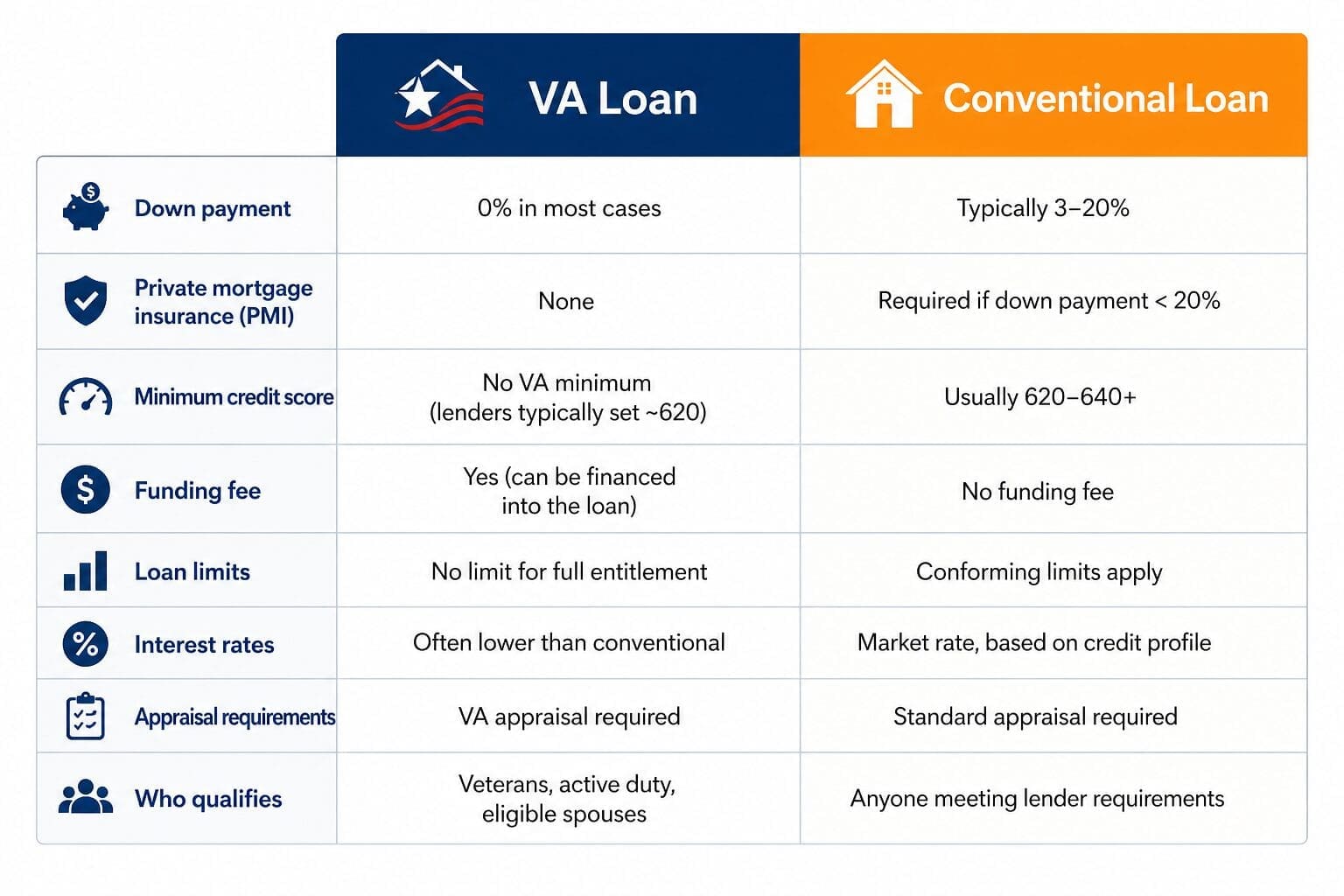

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs. The VA doesn’t lend money directly — instead, it guarantees a portion of the loan, which reduces the risk for lenders and allows them to offer veterans more favorable terms than they might otherwise qualify for.

VA loans are available to active-duty service members, veterans who served the required length of time and were discharged under conditions other than dishonorable, National Guard and Reserve members who meet service requirements, and surviving spouses of veterans who died in service or from a service-connected disability.

If you’re not sure whether you qualify, your Certificate of Eligibility (COE) is the official document that confirms your VA loan entitlement. You can request it through VA.gov, through a VA-approved lender, or by mail.

What is a conventional loan?

A conventional loan is any mortgage that isn’t backed by a government program. Most conventional loans follow guidelines set by Fannie Mae or Freddie Mac, which set standards around credit scores, debt-to-income ratios, and down payments that lenders must meet in order to sell the loans on the secondary market.

Conventional loans are available to anyone who meets the lender’s credit and income requirements — there’s no service requirement. They’re the most common type of mortgage in the U.S.

VA loan vs conventional loan: a side-by-side comparison

The biggest advantages of a VA loan

No down payment required. This is the feature that makes the most immediate difference for most veterans. With a conventional loan, a 20% down payment on a $400,000 home in Massachusetts means coming to the table with $80,000 in cash. With a VA loan, eligible veterans can finance 100% of the purchase price — no down payment required. For veterans transitioning out of service, or anyone who hasn’t had years to accumulate savings, this can be the difference between buying a home now and waiting years to save up.

No private mortgage insurance. Conventional loans require private mortgage insurance (PMI) when the borrower puts down less than 20%. PMI typically adds 0.5% to 1.5% of the loan amount to your annual costs — on a $400,000 loan, that’s $2,000 to $6,000 per year. VA loans don’t require PMI at all, regardless of how much you put down. That’s a significant ongoing savings over the life of the loan.

Competitive interest rates. Because the VA guarantees a portion of the loan, lenders take on less risk — and they typically pass some of that savings on in the form of lower interest rates. VA loan rates are often 0.25% to 0.5% lower than comparable conventional rates, which adds up to meaningful savings over a 30-year mortgage.

More flexible qualification standards. VA loans generally have more lenient requirements around credit scores and debt-to-income ratios than conventional loans. This doesn’t mean approval is automatic, but it does mean veterans who might not qualify for a conventional loan still have a strong path to homeownership.

When a conventional loan might make sense

VA loans aren’t always the right choice for every situation. If you’ve already used your full VA entitlement on a previous home and haven’t restored it, your options may be more limited, and a conventional loan could be the more straightforward path. Similarly, VA loans come with property condition standards — the home must be safe, structurally sound, and sanitary — so fixer-uppers or homes in poor condition may not pass a VA appraisal, in which case a conventional loan or renovation loan might be the better fit.

It’s also worth considering the VA funding fee, which ranges from 1.25% to 3.3% of the loan amount depending on your down payment and whether it’s your first VA loan. Veterans with qualifying service-connected disabilities are exempt from the funding fee. If you have strong credit and savings for a 20% down payment, the numbers on a conventional loan may come out comparable once you factor in the fee — which is why talking to a lender who can run both scenarios side by side is always worth the conversation.

What Massachusetts and Rhode Island veterans should know

The Massachusetts and Rhode Island housing markets are competitive. Median home prices in eastern Massachusetts have climbed significantly in recent years, and inventory in many communities remains tight. For veterans buying in this market, the VA loan’s no-down-payment feature is particularly valuable — it keeps more of your cash liquid, which matters when you’re competing with other buyers or need reserves for closing costs, repairs, or moving expenses.

It’s also worth knowing that Massachusetts has additional veteran-specific homebuying programs that can sometimes be layered with a VA loan, including programs through the Massachusetts Housing Finance Agency (MassHousing). A knowledgeable local lender can walk you through what combinations are available to you.

Your banking relationship matters too

Whether you go with a VA loan or a conventional mortgage, your broader banking relationship plays a role in your financial life as a homeowner. Having a checking account at a bank that understands veteran benefits — VA disability payments, pension deposits, GI Bill payments — means your day-to-day banking is handled by people who understand your financial picture.

At BayCoast Bank, our Honor Checking account is designed specifically for active and retired armed services personnel and veterans. With one direct deposit per statement cycle, the monthly maintenance fee is waived. Maintain an average daily balance above $500 and you’ll earn interest on the account. It’s a small thing compared to a mortgage — but the right checking account, at the right bank, makes everything else easier.

Frequently asked questions

Can I use a VA loan more than once?

Yes. Your VA loan benefit can be used multiple times as long as you have remaining entitlement, or once you’ve restored your entitlement after selling a previous home and paying off the VA loan.

Do VA loans take longer to close?

VA loans do require a VA appraisal, which adds a step to the process. In practice, the difference in closing timelines compared to conventional loans is usually small — often just a few days — when working with an experienced VA lender.

Is there an income limit for VA loans?

No. There’s no maximum income limit to qualify for a VA loan. The VA does look at residual income (money left over after paying monthly obligations), but this is a floor, not a ceiling.

What’s the VA loan limit in Massachusetts?

For veterans with full entitlement, there is no VA loan limit. Veterans with partial entitlement may have limits that correspond to the conforming loan limits in their county.

Is there a checking account designed specifically for veterans at BayCoast Bank?

Yes. The Honor Checking account is built specifically for active and retired armed services personnel and veterans. Set up one direct deposit per statement cycle and your monthly maintenance fee is waived — and if you maintain an average daily balance above $500, you’ll earn interest on your account. It’s a natural home base for your VA benefit payments, whether you’re using a VA loan, receiving disability compensation, or managing retirement pay.

Talk to someone who knows both options

The best way to figure out which loan is right for your situation is to talk to a lender who works with both VA and conventional loans and can run the numbers for your specific scenario. BayCoast Mortgage offers VA Home Loans throughout Massachusetts and Rhode Island, with loan officers who understand the local market and the veteran homebuying process. And when you’re ready to set up the checking account that will receive your VA benefit payments, our Honor Checking account is built with veterans in mind.

BayCoast Bank and BayCoast Mortgage Company serve Massachusetts and Rhode Island. This article is for informational purposes only and does not constitute financial, legal, or mortgage advice. All loans are subject to credit approval. VA loan eligibility is determined by the U.S. Department of Veterans Affairs. Visit VA.gov for official eligibility information.